How to Choose a Financial Planner

Two clients came to us from a large financial services firm. One was a cardiologist in his 40s. The other was an retiree in her mid 70s. From a financial planning standpoint, they couldn’t be more different. He needed a portfolio that secured long-term growth, while she needed a portfolio that provided reliable income. A real financial planner would see this right away and design portfolios to meet their different needs. But the large brokerage firm—to my amazement—had set them up with portfolios that were virtually indistinguishable. Their so-called “advisers” had been selling them the very same financial products. It was clear that these so-called advisers weren’t recommending products that were in their clients’ best interests. They were instead recommending products that paid higher sales commissions to their firm.

Examples like this are all too common in the financial services industry: people looking for a full-time financial planner wind up with a part-time salesperson instead. The reason is that the financial services industry isn’t regulated like other industries.

If you claim to be a medical doctor, you need to have a medical degree and be licensed to practice medicine. Likewise, if you claim to be a lawyer, you need to have a law degree and have passed the state bar exam. By contrast, someone can claim to be a financial planner without being a Certified Financial Planner®. As a result, many people who sell financial products claim to be financial planners even though they’re primarily just salespeople.

To make matters worse, there’s a confusing variety of financial services on offer and an even more confusing variety of labels that financial service providers use to refer to them. The bewildering proliferation of terms makes it difficult for consumers to know what they’re dealing with.

My goal here is to give you the tools you need to separate the wheat from the chaff and find a good financial planner who can meet your needs.

3 TYPES OF FINANCIAL SERVICE PROVIDERS

There are three different types of financial service providers: Robo-advisors, salespeople, and real financial planners.

1. ROBO-ADVISORS

Robo-advisors are firms that use computer algorithms to manage investments. Firms like Betterment and Wealthfront are examples. When you go to a robo-advising firm you have a virtual meeting with someone who fits you into a model investment portfolio that’s managed by an algorithm. The firm charges an annual fee based on the total value of your investments. For example, firms like Betterment and Wealthfront charge an annual fee of about 0.25% of your investment assets.

Robo-advisors can be an attractive option for some people, but it’s important to be aware of their limitations. First, human behavior can undermine their work. The algorithms that manage investment portfolios are typically based on the assumption that people are going to stay invested in the market over the long term. But most investors lack the discipline to stay invested for the long term. They’re inclined to liquidate their investments during the unavoidable ups and downs of the market. As a result, they’re unable to reap any of the benefits a robo-advisor has to offer.

Second, robo-advisors are primarily designed to manage investments. But your financial future depends on a lot more than just investments. It involves a long-term process of continually realigning your financial resources with the goals that matter most to you. That process is what real financial planning is all about.

2. FINANCIAL SALESPEOPLE

Financial salespeople comprise the majority of financial service providers you’ll encounter when you search for a financial planner. Their majority presence in the industry means that many people who are looking for a full-time financial planner end up with a part-time salesperson instead.

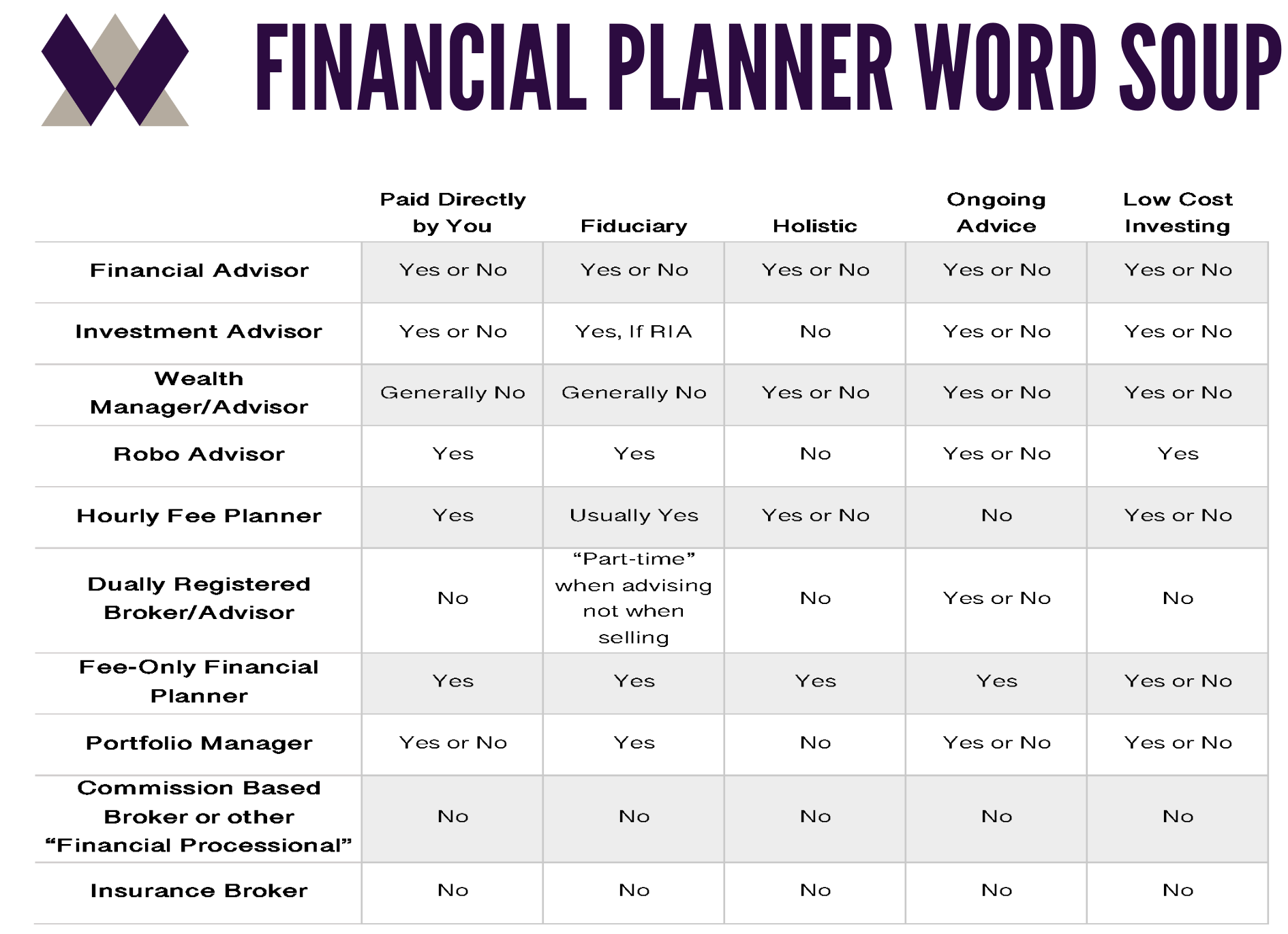

Financial salespeople don’t call themselves “salespeople.” They instead use labels like “wealth manager,” “financial consultant,” or “financial professional.” All of the labels they use—and there are many (see the chart below)—aim at creating an impression that they’re trustworthy, competent, and committed to putting your financial well-being first.

Don’t be fooled by the labels! If a car salesman decided to call himself a “new car consultant,” that wouldn’t change his status as a salesperson. The same is true of financial salespeople. No matter what they call themselves, you have to look past the labels and examine how they’re paid.

3. FINANCIAL PLANNERS

Financial planners are the third type of financial service providers. Financial planning is an ongoing activity that aligns your current financial circumstances with your long-term goals.

It’s important to distinguish financial planning from a financial plan. Financial planning is an activity. It starts from where you are and continuously makes course corrections to ensure you arrive where you want to be. Just as physical fitness is an ongoing process of aligning diet and exercise with long-term health goals, financial planning is an ongoing process of aligning your current financial circumstances with your long-term financial goals.

By contrast, a financial plan isn’t an activity but a thing—usually, a document produced using a computer algorithm. But those algorithms are based on assumptions and predictions about the future—for example, the assumption that the future is going to be just like the past. The problem is that the future is never just like the past. Conditions change. That’s why crystal balls and financial forecasts fail. That’s why people lose at poker and roulette, and why no one can predict the daily ups and downs of the stock market.

To handle the real changes that inevitably occur in life, you need to monitor changing conditions and correct course as required to arrive safely at your destination. That’s what financial planners help you do.

Real financial planners help their clients identify what matters most to them. They help formulate clear and realistic long-term goals, and they help monitor and respond to changing conditions. Unlike robo-advisors, financial planners help keep their clients’ emotions in check through the inevitable ups and downs in the market to ensure their clients achieve the goals that matter most. And unlike financial salespeople, real financial planners are typically paid directly and only by you. In addition, they have a legal obligation to put your financial interests first.

Real financial planners are fiduciaries—a category defined by The Investment Advisers Act of 1940. That Act states that fiduciaries have an “affirmative duty of good faith” to act on behalf of their clients. Real financial planners, in other words, have a legal obligation to put their clients’ best interests first.

Financial salespeople, by contrast, have no such obligation. The law simply requires them to disclose their compensation conflicts to their clients. But those disclosures do nothing to resolve conflicts when they arise (see an example of one of these disclosures here). Think again about the two clients whose so-called financial advisers were selling them products that weren’t in their best interests. Each client had received a disclosure informing them that the firm wasn’t obligated to act in their best interests. But that disclosure didn’t make conflicts of interest magically disappear, and it didn’t protect them from being sold products that benefitted the firm at their expense.

HOW DO YOU CHOOSE A FINANCIAL PLANNER?

When it comes to choosing a financial planner, the first thing to keep in mind is that financial planning is very personal. Over time your planner will know more about you than almost anyone else. That means you’re going to want someone trustworthy, competent, and easy to talk to.

Think, by analogy, of choosing a doctor. You want someone you can trust to put your health first. You want someone who’s competent—who understands what it’ll take to keep you healthy. And you want someone who will talk with you honestly and openly about your health in ways that you can understand.

Similarly, when it comes to managing your money, you want someone you can trust to put your financial interests first, and who views your financial life holistically–who sees your financial well-being as part of your overall well-being. You want someone who’s competent, who understands your financial circumstances–your financial strengths, weaknesses, and long-term goals–and who can recommend concrete steps that will help you achieve those goals. You want someone who continuously monitors your progress toward your goals, and who makes adjustments to keep you on track. And you want someone who will talk honestly and openly with you about your financial circumstances without unnecessary complexity.

Most people start searching for a financial planner in one of three ways: they get referrals from people they know (neighbors, friends, their accountant, or attorney), walk into local financial service establishments, or search the internet. Each of these methods is fine as a starting point, but each has its limitations.

First, recall that financial planning is very personal. As a result, what works for your neighbors, friends, and other people you know, might not work for you. Your goals and financial circumstances, as well as your background and personality, likely differ from theirs. Consequently, the best financial planner for them might not be the best planner for you.

Second, local financial service establishments often represent large firms like Edward Jones or Merrill Lynch. The problem with most large financial service firms is that they tend to focus on selling investments instead of planning your financial future. Their websites use all the right phrases like “focusing on life priorities” and “personalized planning.” But in reality, they tend to view financial planning as a distraction. They’re paid sales commissions from investments, so selling investments is their primary business.

Third, Google searches tend to steer people in the direction of financial salespeople. Recall that salespeople make up the majority of financial service providers. Recall, moreover, that those salespeople typically don’t call themselves “salespeople.” That means you need to exercise caution when examining the services they offer.

Here are seven tips to help you find a real financial planner who’s right for you:

- Look up the firm using the FINRA Broker Check. FINRA is an independent entity that plays an important role in financial services by promoting transparency and disclosure by brokers and advisors. Its Broker Check provides summaries of the backgrounds, regulatory actions, and complaints about people at a firm.

- Look for disclosures on the firm’s website. If the website of a financial services firm has disclosures like the one described here, you should probably look elsewhere. Otherwise, you might end up with a financial salesperson instead of a financial planner.

- Look for a firm that provides financial planning, not just static computer-generated financial plans. Recall that financial planning is an ongoing activity; it’s not something that’s just “one and done.” You want a financial planner who’s going to continuously help monitor your financial circumstances and help make adjustments when necessary. You don’t want a static document generated by a computer algorithm that’s based on guesses about the future.

- Beware if your first conversation with a financial firm focuses on investments. If you talk to someone at a financial services firm, and the initial discussion focuses on investments, this can be a red flag. Investments are important, but there’s a lot more to financial well-being than just investments. Helping manage your behavior and your expectations is more important to securing successful long-term outcomes. The best investments in the world can’t save you from financial decisions that are impulsive or reactive. Helping keep your emotions in check is one of the most valuable services a financial planner can provide.

- Ask whether your financial service provider is a full-time fiduciary. Recall that fiduciaries have a legal obligation to act in their clients’ best interests. Knowing that a financial service provider is a fiduciary provides you with some measure of confidence that they’ll be putting your financial interests first.

- Ask how your financial service provider is paid. How a service provider gets paid can reveal whether or not they’re a financial salesperson masquerading as a financial planner. Real financial planners are typically paid directly by you. If, by contrast, a financial service provider’s payment is “fee-based,” that’s typically code for being paid on commission, which is an indication that you’re dealing with a financial salesperson.

- Ask these questions: What’s your definition of a financial planner? Why did you become a financial planner? What type of clients do you have? The answers to these questions will help you understand how the financial planner views their role and whether they’re the right person to help you accomplish your goals.

Sooner or later you’ll probably need a financial planner—whether it’s to help plan your retirement, handle a recent inheritance, or save for future college expenses. You want to work with a planner who’s trustworthy, competent, and a good communicator. You don’t want someone who’s angling for their own gain, who’s focused on commissions, or who sees every financial planning issue as an opportunity to sell you something. Finding a trustworthy and competent financial planner may not be easy, but it’s worth the trouble once you find a good fit. Don’t settle for someone with an agenda different from yours. We’re here to help when you need us. Ready for a real conversation?