Inflation: Perception Versus Reality

Because of increasing inflation, you will need more money this year to pay for your lifestyle expenses. The average American will need $5200 more in 2022 to meet expenses according to Bloomberg Economics.

Inflation occurs when prices for goods and services are increasing; this means that the purchasing power of your money is decreasing.

Over the past century, inflation has averaged around 3% per year; the past 20 years have been less than 2% per year. That’s then and this is now – inflation is currently running at an annual rate of 8.5% and could go even higher.

WHY INFLATION IS PERSONAL

Inflation is notoriously difficult to measure; your personal inflation rate might be higher or lower than the “headline” inflation rate. If you aren’t buying a house or renting an apartment, the portion of inflation attributable to real estate doesn’t apply. Conversely, if you consume more energy or food versus the inflation index, your personal inflation rate will be higher.

The increase in oil prices, which commenced early last year, but accelerated a few months ago, accounts for over half of the total rate of inflation at present.

You can easily get lost in all the reasons for the inflation uptick, but you should remember that sustaining your lifestyle after inflation is the fundamental reason for investing and taking risk in the first place.

Market history shows that stocks are an efficient long-term hedge against inflation. Short-term stock market returns might differ, but the long-term record is unassailable.

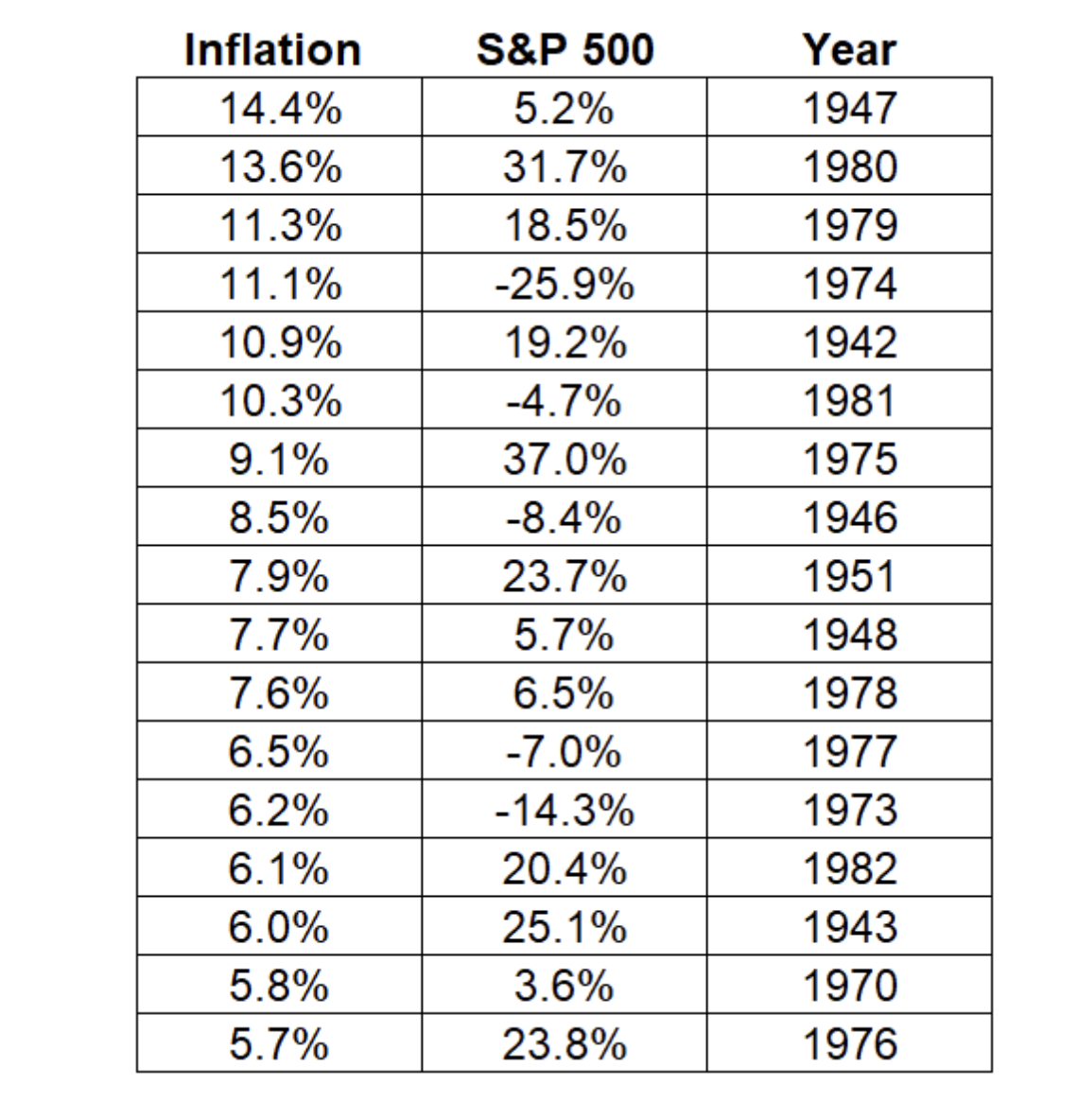

The table below depicts the highest inflation years since 1943 along with the S&P 500 returns for those years.

The S&P 500 averaged 9.4% per year for these high inflation years, fairly close to the long-term average of 10% per year. The S&P 500 posted double-digit returns in eight of the 17 years – with six years producing annual returns over 20%.

HOW TO ADJUST YOUR INFLATION MINDSET

Inflationary psychology can create significant difficulties for consumers, businesses, and policymakers. A dangerous inflationary cycle can develop as consumers speed up purchases in anticipation of higher future prices and businesses raise prices for the same reason.

The government has a poor record of combating inflation. President Nixon instituted wage and price controls in 1971 when inflation was just beginning to heat up. This effort was largely unsuccessful. Undeterred, President Ford followed in 1974 with his infamous WIN (Whip Inflation Now) initiative with inflation running at an annual rate over 11%. Neither of these materially altered the perception or reality of inflation.

Once inflation psychology takes hold and prices actually increase, these price increases tend to be “sticky” as Professor Eugene Fama says. You can see on the table above that higher rates of inflation sometimes endure for 2 or 3 years or longer.

While no one knows how long the current inflation uptick will last, you should begin developing an inflation mindset. Look at your short-term spending and how this meshes with your long-term priorities. Think about tradeoffs and choices you can make to improve your overall financial picture. Start there. Ready for a real conversation?